Frequently Asked Questions

Answers to your Frequently Asked QuestionsYour insurance should suit your unique needs. Whether you are already a TAL customer or thinking about joining us, we want to make sure you have all the information you need to make an informed choice about your insurance.

The below frequently asked questions are intended as a guide only, and you should consider your own objectives and financial situation when purchasing insurance cover. If you can’t find what you’re looking for then contact our specialists.

General

What does life insurance cover me for?

What additional features of TAL Accelerated Protection can I set up over the phone?

I have life insurance as part of my super, is that enough?

Can I increase my insurance cover?

I’ve changed my address or contact details – how do I let you know?

Will my payments be taxed?

What is Inflation Protection?

What is a standalone policy?

Who is TAL?

Who is Dai-ichi Life?

How can Workers’ Compensation payments affect my insurance payouts?

Can I cancel my policy if I no longer need it?

Claims

What happens after I submit my claim forms?

How will I or my family receive payments?

What is a qualifying period for Total Permanent Disability (TPD)?

What is the Waiting Period for Income Protection?

My Income Protection claim has been approved. When will I start receiving payments?

Can I earn other income while I’m receiving Income Protection payments?

What can I do if I don’t agree with TAL’s decision about my claim?

Can I request that the decision is reviewed?

Can I get a copy of the documents in my TAL claim file?

How can I request information from my TAL claim file?

Can I provide feedback to you about my claims experience?

If my partner is the beneficiary of my life insurance and we both pass away, what happens to my benefit amount?

Do I need to update the insurer if my health or occupation changes?

If I make a claim do my premiums increase?

Do I need to continue to pay my premiums if I was to go on claim?

What happens to my insurance benefit through super if I do not make a binding nomination?

What is the difference between a non-binding nomination and a binding nomination?

Can I hold Critical Illness and Trauma Insurance through my super?

What if the condition I claimed for is excluded from the policy?

What happens to my policy if I was to move overseas?

Tax time

What is an Income Protection Summary?

When will my IP summary become available?

Am I eligible to register for myTAL?

How can I access my IP Summary?

My policy is eligible to register for myTAL. How do I register?

Will I receive a payment summary for my Life Insurance, TPD or Recovery Insurance policies?

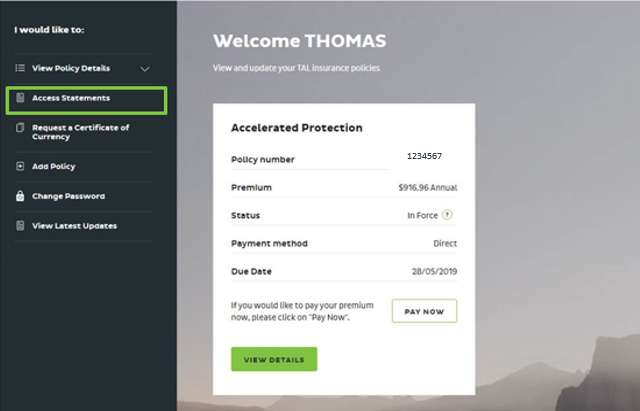

I’ve registered for myTAL. How do I download another copy of my IP Summary online?

A copy of your Income Protection summary is expected to be available for quick download from the 28 July 2023. To access yours follow the steps below:

- Login to MyTAL

- Select ‘Statements’ on the left-hand menu

- Select a policy from the policy drop down box

- Select the statement from the statement from down box

- Click on the statement you would like to download

- If you do not see the statement you would like to download click on the ‘Show More’ link’

- Select the financial year you would like to request a statement for, enter your email address and click the button ‘Request PDF Tax Statement(s)’