What should you consider when choosing a Life Insurance beneficiary?

Money Management -

When taking out a life insurance policy, it’s important to consider who should be your life insurance beneficiary and the role they play.

What is a life insurance beneficiary?

A life insurance beneficiary is the person who will receive your life insurance payment should you pass away.

When choosing yours, it’s important to think about who you would want to financially take care of should something happen to you. For most people, this is their spouse or children.

If you’re yet to nominate your beneficiary for your TAL Life Insurance, you can easily do so.

Nominating a beneficiary may seem straightforward, but there are a number of things to be aware of and plan for.

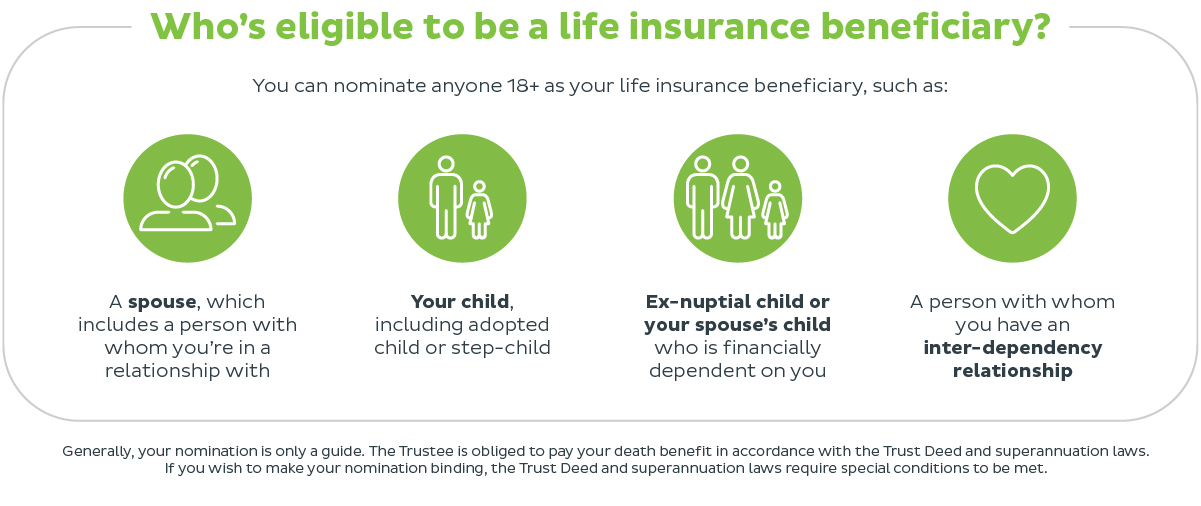

Who can be a beneficiary?

It’s important to consider that if your beneficiary has any debts the proceeds might be used to pay them off. As well as this, keep in mind that if you nominate a minor such as your children, they will only receive the full amount once they turn 18.

Naming a beneficiary ensures your benefit is not paid to your estate and goes directly to the person you nominate.

Can you have multiple life insurance beneficiaries?

You can easily name multiple people as beneficiaries to your policy – you can check with your insurer as to how many beneficiaries can be named on your policy.

If you do decide to choose several people, it’s useful to designate a percentage of the payment to each person, as opposed to a specific amount (as this may change).

You should also consider having a contingency beneficiary, should a primary beneficiary pass away before or around the time of your passing (for example, in an accident).

What to do if you don’t have a beneficiary

If you hold the policy in your name, your benefit will go to your estate and be managed as part of your will.

If you have outstanding debts when you pass away, your benefit may be used to pay them before it is distributed to the people named in your will – this means your loved ones could miss out on the payment.

What’s the difference between a binding and non-binding beneficiary?

If you have life insurance within your super, you’ll be asked to nominate a beneficiary – a family member or loved one who will receive the life insurance money if you pass away. You have the choice to make a binding or a non-binding nomination.

A binding nomination is a legally binding statement which your insurer will use to know who your money should go to if you pass away.

A non-binding nomination is not legally binding. Your insurer will take your non-binding into consideration when making the life insurance payment on your behalf, in addition to other aspects of the law.

To ensure your family is looked after when you’re not around, it’s important to keep your beneficiary details up to date within your super account.

How to keep your beneficiary up to date

You should evaluate your beneficiary and policy at any major life event – for example, purchasing a home, having children, getting married, getting divorced or at the death of a loved one. Having life insurance beneficiaries up to date ensures your loved ones are taken care of financially if something were to happen to you. Remember, you can easily update your policy and beneficiary through myTAL. And if you have any further questions concerning beneficiaries, feel free to contact your Financial Adviser or the TAL team.

Don't have life insurance? Get a quote today.

Get a quote