Foundation 1: Have a spending plan in place

Financial health

Helping Australians understand the importance of good financial health.

The connection between your financial, physical and mental health is greater than you may realise. Which is why, when we look at health, we take a holistic approach: because the balance of physical, mental, and financial health is key to overall health and wellbeing.

What is financial health?

Your financial health takes into account several factors relating to your personal financial situation including the amount you have in savings, how much you are putting away for retirement and how much of your income you are spending on fixed or non-discretionary expenses.

Another way to look at it is having the financial security to provide financial freedom now and into the future.

Why good financial health matters?

Aside from the impact on overall health, good financial health can have a profound impact on people and their ability to provide for themselves and their family into the future.

At TAL we want all Australians to enjoy the freedom that comes with being financially healthy, that’s why we’ve partnered with Glen James, a former financial adviser and host of the My Millennial Money podcast to help educate Australians on the importance of having good financial health and steps to take in order to have a good financial future.

"As a retired financial adviser, I've seen what does and doesn't work when it comes to money. I developed the Sound Financial House to explain to clients how to get set up in your financial life, and in what order. This Sound Financial House is a visual representation of the financial foundations you need to continue building to set up, protect and grow your wealth."

- Glen James

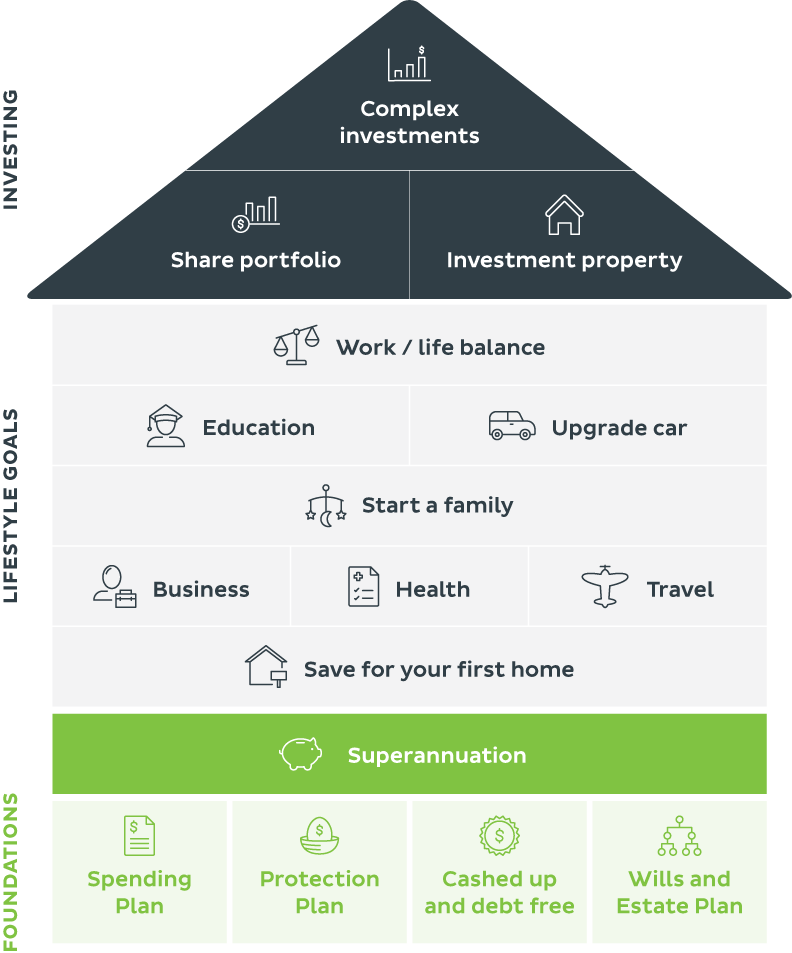

A sound financial house with Glen James

Investing in the future is important, but when it comes to your finances you need to do things in the right order. Before investing, you need to make sure you have solid financial foundations. Glen’s sound financial house shows you how to set up the structure of your money life, illustrated in an easy to understand way – it’s like building a house.

Building your sound financial house

You can’t build the roof of a house without the frame, and you can’t build any of the house frame without solid foundations.

Join Glen James and John Pidgeon as they discuss millennial money matters in a light-hearted way.

Disclaimer: Any financial product advice is general in nature only and does not take into account any person’s objectives, financial situation or needs. Before acting on it, the appropriateness of the advice for any person should be considered, having regard to those factors. Persons deciding whether to acquire or continue to hold life insurance issued by TAL should consider the relevant Product Disclosure Statement (PDS). The Target Market Determination (TMD) for the product (where applicable) is also available. Life insurance issued by TAL Life Limited ABN 70 050 109 450 AFSL 237848.